Health insurance costs continue to put pressure on family budgets in Georgia, and even when premiums are not the highest in the country, many households here still feel the strain more sharply than families in other states. Nationally, the average annual premium for employer-sponsored family coverage reached $26,993 in 2025, with workers paying an average of $6,850 of that total out of pocket. At the same time, workers’ wages rose 4% while family premiums rose 6%, meaning insurance costs are still growing faster than paychecks.

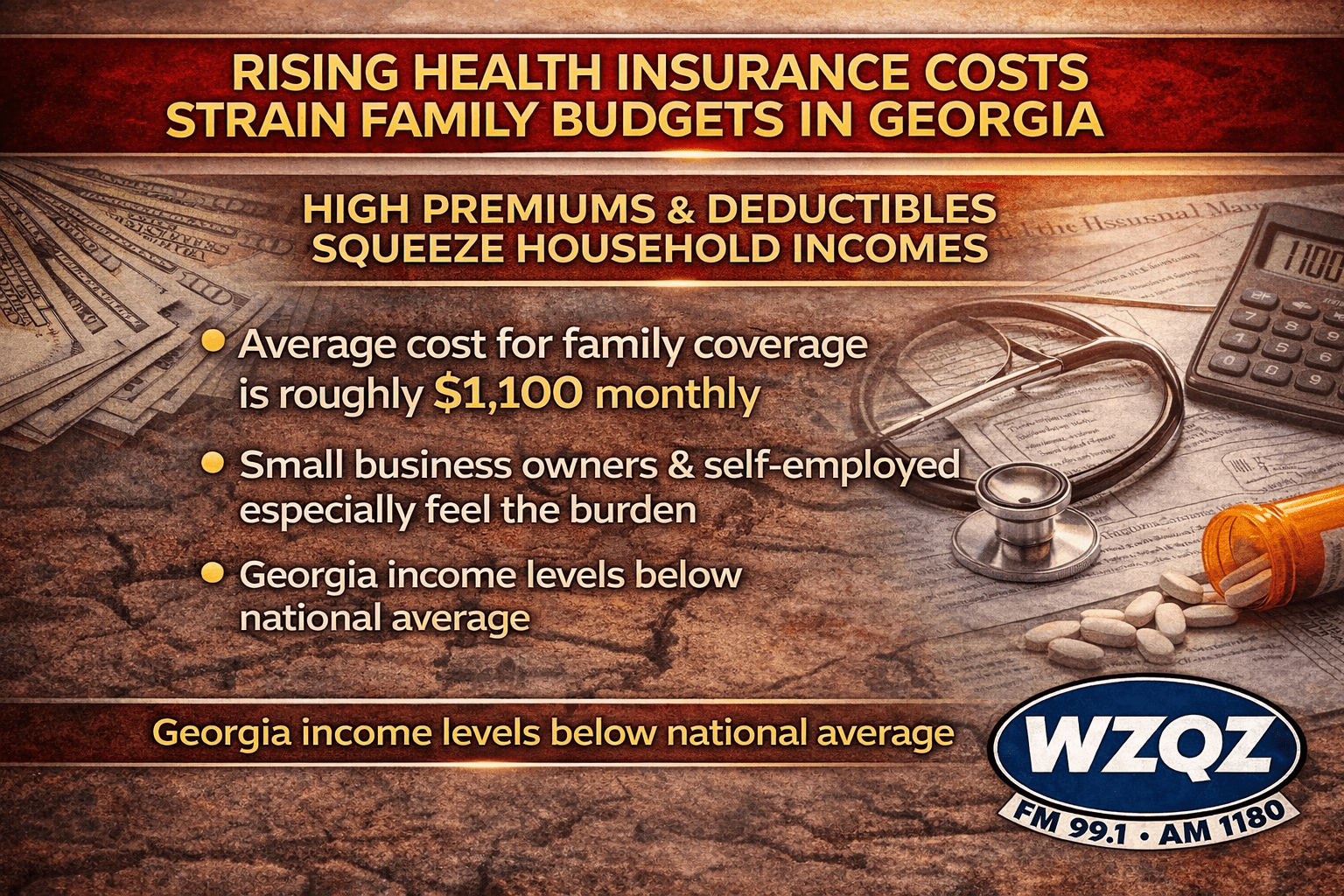

For Georgia families, that squeeze can be even harder because household income in the state trails the national figure. Census income data show Georgia’s 2024 median household income was $81,210, compared with $83,730 nationally. When a large monthly premium, deductible, copays, and prescription costs are stacked on top of housing, groceries, transportation, and child care, health coverage can take a bigger bite out of a Georgia paycheck than the national averages alone might suggest.

That reality affects everyday family decisions. A higher insurance bill can mean less room in the budget for savings, school expenses, home repairs, or even routine doctor visits. Even households that do have coverage often face deductibles before insurance fully starts paying, and KFF reports the average deductible among covered workers in a plan with a general annual deductible was $1,886 for single coverage in 2025. For many families, the issue is not just whether they have insurance, but whether they can comfortably afford to use it.

The burden can be especially heavy for self-employed Georgians, who do not have an employer helping cover the premium. Federal health policy analysts say ACA marketplaces created an important source of coverage for people without access to affordable employer plans, including small business owners and self-employed workers, and Treasury data cited by HHS show 3.3 million small business owners and self-employed adults obtained marketplace coverage in 2022. But for many of those workers, the full cost of coverage still comes straight out of household income, making monthly premiums a direct business and family expense at the same time.

Farmers in Georgia face a similar challenge, especially because farming is so often tied to self-employment and irregular income. USDA says most insured Americans get coverage through employers, and farm households are no exception, but it also notes that time demands on the farm can prevent many farmers and ranchers from accessing employer-sponsored insurance through an off-farm job. That leaves many farm families relying on individually purchased coverage or a spouse’s job for insurance, which can become difficult in years when crop prices, livestock markets, or weather conditions squeeze farm income.

Small business owners are also caught in the middle. They have to decide whether they can afford coverage for employees while also paying for their own families’ care. NFIB says the cost of health insurance has been the number one long-term small business problem identified by its members for nearly 40 years, and 98% of small employers offering coverage say they are concerned that the cost will become unsustainable in the next five to 10 years. Georgia does offer SHOP coverage for small businesses with up to 50 employees, and some may qualify for a federal tax credit, but the challenge remains steep enough that many owners still see insurance as one of their biggest cost pressures.

The broader backdrop is that Georgia still has a relatively high uninsured rate. America’s Health Rankings, using 2024 Census data, puts Georgia’s uninsured rate at 12.0%, and Census reporting shows uninsured rates rose in many states between 2023 and 2024. When coverage is expensive or hard to obtain, more families are left exposed to the risk of large medical bills, and even insured families may delay care because of what it will cost.

The bottom line for Georgia is that health insurance is not just a healthcare issue. It is a kitchen-table budget issue. For working families, the self-employed, farmers, and small business owners, the rising cost of coverage can shape everything from hiring decisions to grocery spending to whether someone goes to the doctor at all.

Comments